Stress testing and capital adequacy in banking: tackling the technology challenges

Need to know

This Point of View article provides context for a webinar held by Chartis and Appian on October 24, 2023.

Stress testing – an overview

In stress tests, banks develop and apply specific scenarios to assess the impact of shocks to the financial system. Following the 2007-8 financial crisis, the focus of the financial industry intensified on stress tests as a method of ensuring that banks have adequate capital buffers in the event of shocks to the system. The aim of stress testing regimes is to prepare banks to absorb financial shocks, and to ensure they can continue to provide credit to the economy during periods of market stress.

While stress tests vary in the scope, methodology and granularity they require, they share broad macroprudential and microprudential principles, and require data from a wide range of business lines and asset classes that a bank may hold. Stress tests also tend to be based on statistical tools and techniques that rely on large amounts of data from sources that include balance sheets, operations, credit portfolios, and liquidity and market risk data. And as the availability and granularity of data has increased over time, so has the depth and scope of information required by regulators to capture risks and pinpoint stresses.

Notably, however, while very large banks are data-rich, smaller institutions haven’t yet captured enough data to give them an accurate understanding of liquidity risk. Consequently, from a regulatory standpoint, different banks must be able to view their deposits differently.

Remaining relevant

Supervisory stress tests have clearly been a vital innovation following the financial crisis. Since then, while their core principles have remained constant, stress testing frameworks have evolved to embody new and emerging risks, as well as amendments to capital and eligibility criteria.

But stress testing as a discipline must continue to evolve to become more dynamic. Ultimately, the aim of stress testing regimes is to remain relevant – the policymakers and economists who devise stress tests are tasked with staying ahead of the evolving financial system and risk management landscape, as well as emerging risks such as climate risk.

Stress testing the global banking sector

Many financial institutions have less than $100 million in assets, and while regional markets can differ, these tier-two banks all share similar challenges in terms of their efficiency, internal operations, costliness and data management. Many of them, for example, tend to be branch-oriented and employ relatively large numbers of people.

Technology can help them create internal efficiencies, by automating manual processes to increase the volume of work and reduce the risk of human error. Digital channels continue to be an area of strong opportunity, but for community and regional banks they can also present the biggest challenges, and even threats.

Notably, for many institutions, the current inflationary environment creates the potential for stress testing models to miss what’s happening in the marketplace. Inflation is not typically built into models, which have traditionally relied on historical data. This has created opportunities for institutions to develop stress testing models that can manage these risks.

The challenge for smaller banks

Crucially, while smaller banks’ ability to develop their own technology is limited compared to that of larger institutions, continued technology investment, both internally and customer-facing, is essential. The need to innovate and implement smart technology is greater than ever, and many financial institutions are starting to shift their focus to artificial intelligence (AI) to increase their scope.

But in an environment of fast consolidation and heavy competition, smaller banks face technological challenges: attaching and incorporating agile tech is no trivial task. In the current environment, smaller firms must consider some vital market dynamics to succeed:

- More competition will be needed to enhance their performance and success.

- More products that incorporate AI will become available to them. A lack of appropriate in-house tech means that they won’t be at the bleeding edge. Nevertheless, these tools can help to enhance their internal efficiency by, for example:

- Addressing issues of bias in lending.

- Improving their data. Bad data can have a serious impact on the effectiveness of models; being able to understand and track data lineage and improve its validity is vital. Robust data is also essential for uses of GenAI: even these models are only as good as the data fed into them.

- Introducing basic automation to tackle many processes that are still manual, helping to reduce risk.

- Creating a process that can gather significant volumes of data effectively and efficiently, while managing costs and scale.

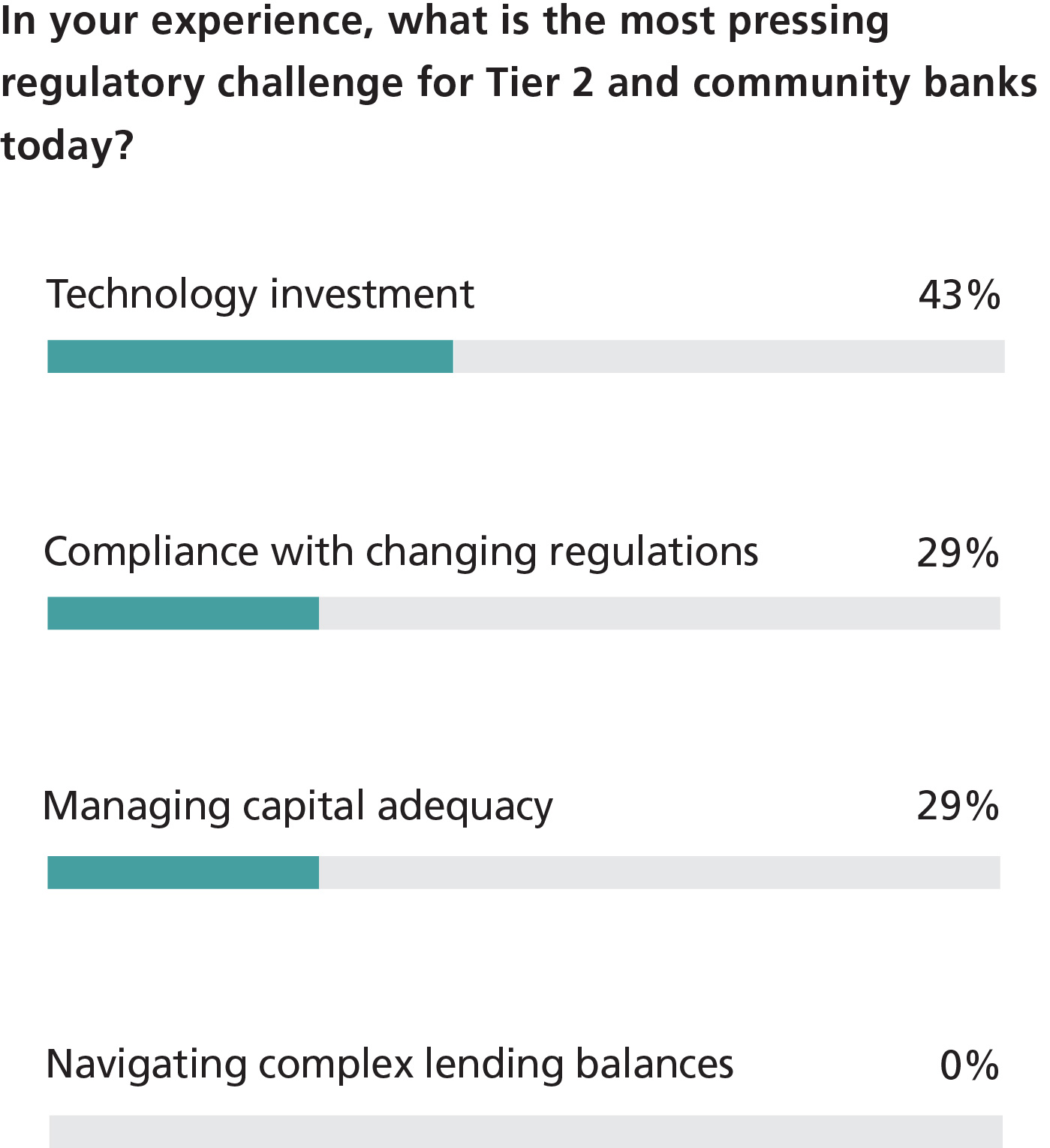

To explore some of these issues, we conducted a short poll of attendees to the webinar. Some of the results are shown in Figures 1 and 2. While these are not statistically significant, they do highlight the importance of advanced technology tools, and give us a sense of the pressing challenges facing banks today.

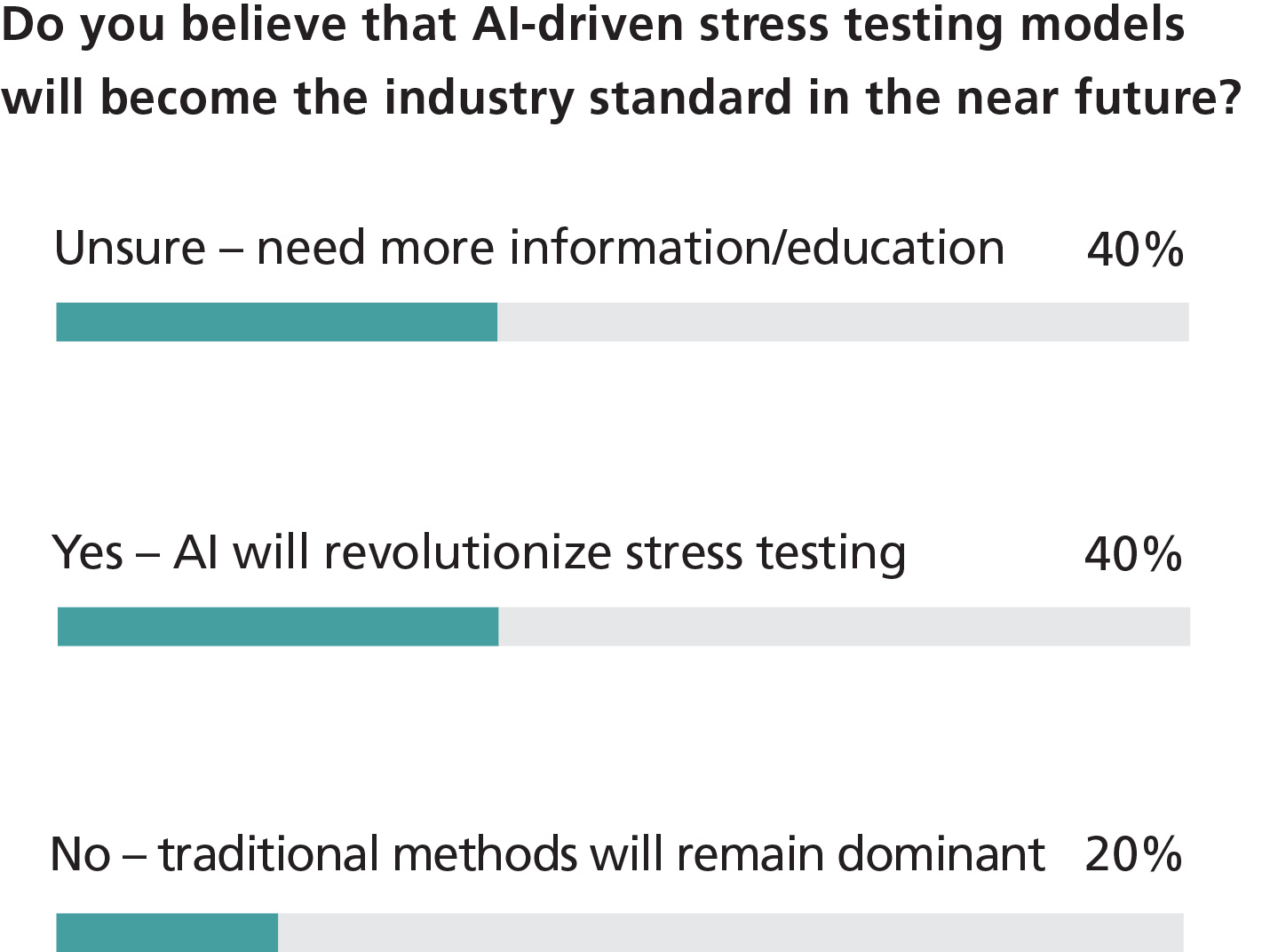

Notably, when asked about the impact of AI on stress testing (see Figure 2), 40% of those polled said they were uncertain about it and needed more information. Clearly, selecting the right solution is predicated on knowing what problem it is you’re trying to fix, and how that might change. This need for capabilities and flexibility is at the heart of the issue. So while AI may make sense for stress testing, better definitions and more information are crucial.

Figure 1: Poll results – regulatory challenges and technology

Source: Chartis Research/Appian

Figure 2: Poll results – AI in stress testing

Source: Chartis Research/Appian

Meeting the challenges

Selecting the right technology while regulations continue to change is one of the biggest challenges facing banks. Institutions that are tied to traditional core processing systems are also encountering challenges in offering the technology tools and systems that customers increasingly demand. To develop effective stress testing and operational systems, firms must have technology that can be adapted quickly, and which is cost-effective and up to date in terms of regulatory requirements.

There are plenty of options to choose from. While GenAI systems show promise, there are other, more basic technologies that institutions both big and small can focus on in the meantime. Legacy and traditional financial intuitions can leverage apps and other low-code platforms to ensure that their offerings and operations become and remain agile.

First these institutions must carefully consider their strategy if they are to create an enterprise that’s future-proof. Operationally, they must start by assessing their own systems. Then they must consider what tools they can leverage to help them execute on their tech approach – and then ensure that this approach aligns with their enterprise strategy.

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@risk.net or view our subscription options here: http://subscriptions.risk.net/subscribe

You are currently unable to print this content. Please contact info@chartis-research.com to find out more.

You are currently unable to copy this content. Please contact info@chartis-research.com to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@chartis-research.com

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@chartis-research.com

More on Custom Insights

Regulatory reporting: deployment options and managed services

A collaborative article by Chartis and Regnology

Reimagining Model Risk Management: New Tools and Approaches for a New Era

A collaborative report by Chartis and Evalueserve

A New Regime: The Future of Private Credit and Risk Management Needs

A collaborative article by Chartis and RiskSpan

Regulatory reporting: the transition from in-house to third-party systems

A collaborative article by Chartis and Regnology

Keeping good company: streamlining client onboarding with CDI – Part 3

A collaborative article by Chartis and Encompass

Keeping good company: streamlining client onboarding with CDI – Part 2

A collaborative article by Chartis and Encompass

Keeping good company: streamlining client onboarding with CDI – Part 1

A collaborative article by Chartis and Encompass