EMS vendors must eliminate transaction fees and make multi-broker, multi-asset trading easier

Execution management systems (EMSs) profess to be multi-broker and multi-asset, yet traders are still juggling multiple EMSs on their desktops. There is a threshold effect at work, whereby EMSs’ penalizing transaction fees and workflow inefficiencies undermine performance claims.

Transaction fees kept secret

EMSs need to support multiple brokers and assets, to help traders optimize their use of valuable desktop real estate and minimize workflow inefficiencies. But some EMS vendors undermine their multi-broker, multi-asset claims by charging brokers penalizing transaction fees that are ultimately passed onto the buy-side as higher than average commission rates. Anecdotal evidence shows that these transaction fees alone can easily exceed $1 million per year for a global asset manager with multiple regional broker connections – in addition to standard fixed monthly connectivity fees.

When choosing an EMS vendor, buy-side firms typically go through a lengthy request for proposal (RFP) process, but transaction fees are kept secret with strict non-disclosure agreements. Buy-side traders are often unaware of the real impact that transaction fees can have on their workflow processes. Only after an EMS vendor has been selected, and contracts are signed, will the buy-side firm start to become aware of the transaction fees being passed through to it. Often, traders will try to minimize these transaction-cost pass-throughs by connecting to some brokers via other cheaper, multi-broker-friendly EMSs that do not charge transaction fees. But this option is far from ideal, as it forces traders to balance two, three or more EMSs on their desktop. In an age where trade-cost transparency is paramount, this secretive transaction fee-charging is surprising at best.

Independence and multifunctionality

Some EMS vendors further undermine their multi-broker, multi-asset claims by giving preference to default brokers, in terms of functionality and ease of use. This is where the value of having a truly independent EMS comes to the fore. The ease of use and functionality of order tickets, for example, can vary significantly. Compared to other brokers on the network, default brokers’ tickets can be equipped with more ‘bells and whistles’ and greater functional sophistication. Ease of access to strategy saving tools and other functionality may also be reserved only for default brokers.

In some instances it has been demonstrated that certain portfolio trading functionality is only available for default brokers but not for other brokers on the network. Monitoring tools and fields can also vary significantly between preferred brokers and others. And at times it can be troublesome to engage in portfolio trading with brokers that have order tickets set up on the platform which are not designed to be fully integrated with the portfolio trading blotters, monitors and workflow processes.

Multi-broker, multi-asset trading: a case study

A buy-side firm traded with only one broker for years, but was recently offered an opportunity to ostensibly reduce its trading costs by adding a broker that charged a significantly lower commission rate. The head trader asked the firm’s EMS vendor to add the new broker, and it facilitated the request promptly. But the head trader soon encountered problems:

- Transaction fees. The EMS vendor charged the broker a transaction fee that was close to the commission rate charged for execution and clearing services. This was in addition to the set-up and monthly connectivity fees charged to the broker.

- Workflow inefficiency. The EMS order ticket for the added broker did not offer the same functionality as the default broker’s ticket.

To address the first problem, the head trader and broker negotiated with the EMS vendor, and the broker raised its commission rate until a compromise around pricing was reached. The second problem, however, was more complicated. The new broker’s order tickets were not fully integrated with the portfolio trading blotters, resulting in a more difficult trading experience. In the end, the EMS issues forced the head trader to stop trading with the lower-cost broker.

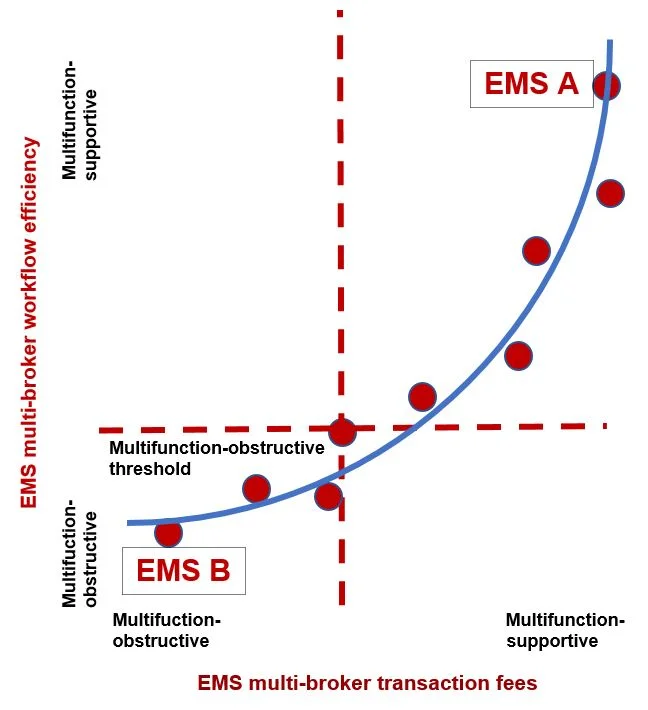

The EMS threshold effect

In theory, many EMS solutions support multi-broker, multi-asset functionality. In practice, however, there appears to be a threshold effect at work. Figure 1 illustrates this ‘multifunction’ threshold effect, whereby an EMS vendor crosses the line from supporting multiple brokers to obstructing multi-broker operation. We consider two EMS vendors, EMS A and EMS B.

-

EMS A is multifunction-supportive, placing in the top-right quadrant of the multi-broker threshold-effect chart. It charges brokers a nominal flat monthly connectivity fee, and no transaction fee. It also has an order ticket that operates the same across all brokers connected to the platform. The same monitoring fields in its order and execution blotters are available to all brokers on the platform. In addition, its portfolio and pair-trading functionality and workflow processes are identical across all broker connections.

-

EMS B is multifunction-obstructive, placing in the bottom-left quadrant of the threshold chart. It charges brokers a sizeable fixed monthly connectivity fee, and tacks on an additional, and sizable, transaction fee. In some cases, EMS B’s transaction fee could be close to the commission rate charged by the broker to execute and clear the trades. EMS B also has an order ticket that is easy to use for default brokers, but not for other brokers on the network. Equally, its order and execution blotters have monitoring fields that operate for some brokers but not for others. In addition, the solution’s portfolio and pair-trading functionality may only be available to some brokers.

Figure 1: The EMS multifunction threshold effect

Source: Chartis Research

While this comparison is a simplified thought experiment, it highlights the very real problems faced by many buy-side traders and their brokers in this area. It also helps to emphasize the role that EMS vendors play, as investment managers attempt to achieve best execution in line with their regulatory requirements.

The EMS role in best execution

Best execution is an evolution, but easy access to liquidity sources has always been a key part of the trading process. When the Regulation National Market System’s (Reg NMS’s) order protection rule was established in 2005, requiring access to an array of liquidity providers, it ushered in a new era in best execution. Then, in 2018, Markets in Financial Instruments Directive II (MiFID II) took the concept of best execution to a higher plane, by requiring buy-side firms to take ‘all sufficient steps’ in the best interest of their clients. In addition, Regulatory Technical Standard (RTS) 28 requires managers to publicly disclose best-execution policy reports that reveal the quantitative and qualitative factors they consider when making venue and broker-routing decisions.

EMSs play a crucial role in helping buy-side firms achieve best execution, by providing access to exchanges, venues and brokers. EMS vendors that frustrate buy-side firms’ efforts to connect to their panel of optimal execution brokers, across regions and asset classes, could be viewed as obstructing their clients’ efforts to achieve best execution.

Further reading

Future Chartis research on market structure will address the key technology trends that are of ongoing importance for buy-side investment managers. These include transaction cost analytics, execution algorithms, smart order routing, artificial intelligence and machine learning, order management systems, execution management systems, securities exchanges, alternative trading venues, bank capital and liquidity, and in-house vs. outsourced trading.

Chartis plans to publish an in-depth EMS market quadrant report in Q1 2021.

Hedge Fund Risk Management Technology, 2018

(Chartis, 2018)

Risk as a Service for the Buy-Side, 2018

(Chartis, 2018)

Points of View are short articles in which members of the Chartis team express their opinions on relevant topics in the risk technology marketplace. Chartis is a trading name of Infopro Digital Services Limited, whose branded publications consist of the opinions of its research analysts and should not be construed as advice.

If you have any comments or queries on Chartis Points of View, you can email the individual author, or email Chartis at info@chartis-research.com.

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@risk.net or view our subscription options here: http://subscriptions.risk.net/subscribe

You are currently unable to print this content. Please contact info@chartis-research.com to find out more.

You are currently unable to copy this content. Please contact info@chartis-research.com to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@chartis-research.com

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@chartis-research.com

More on Points of View

No surprises: 2025 will be another big year for AI

Last year was revolutionary for AI, with potentially far-reaching impacts, and 2025 looks set to offer more of the same, with perhaps some sobering lessons. Taking a pragmatic view, Maryam Akram, Research Principal at Chartis, offers some predictions for…

Regulatory reporting: deployment options and managed services

A collaborative article by Chartis and Regnology.

Reimagining Model Risk Management: New Tools and Approaches for a New Era

A collaborative report by Chartis and Evalueserve.

A New Regime: The Future of Private Credit and Risk Management Needs

A collaborative article by Chartis and RiskSpan.

Regulatory reporting: the transition from in-house to third-party systems

A collaborative article by Chartis and Regnology.

Keeping good company: streamlining client onboarding with CDI – Part 3

A collaborative article by Chartis and Encompass.

Keeping good company: streamlining client onboarding with CDI – Part 2

A collaborative article by Chartis and Encompass.

Keeping good company: streamlining client onboarding with CDI – Part 1

A collaborative article by Chartis and Encompass.