The Japan tick-size harmonization and best execution problem

In 1996, the Financial System Reform Law (the so-called ‘Japanese Big Bang’) aimed to modernize Japanese capital markets, guided by the principals of fair competition. On 2 June 2021, a working group for the Japan Financial Services Agency (JFSA) called for a change to the country’s best execution policy that would force retail order flow off the primary Tokyo Stock Exchange (TSE) in favor of off-exchange Proprietary Trading Systems (PTSs), driven purely by differences in quote tick-sizes. We believe that this new rule, if instituted fully, will soon put market share for the PTSs on a trajectory to overtake that of the TSE. We propose quote tick-size harmonization, as in the US and Europe, [1] in the interests of fostering fair competition, best execution and trust in Japan’s financial institutions.

Context and background

In December 1998, Japan’s Securities and Exchange Law was revised to abolish the ‘concentration [of trading on the exchanges] rule’ and allowed registered PTSs to compete directly with the exchanges.[2] In 2001, Instinet became the first foreign financial institution to establish a PTS in Japan, competing directly with the TSE. Then, in 2006 and 2010, various US financial powerhouses established and took ownership and market-making operations stakes in the PTSs Japannext and Chi-X Japan, respectively.

In the early days of PTSs’ market development, many participants believed that the market share of these systems would grow rapidly, because regulators had allowed them to provide clients with cheaper prices, relative to the TSE, by offering smaller quote tick-sizes. But Japan’s approach to best execution policy has traditionally allowed market participants to consider multiple ‘best terms’ trade lifecycle factors that go beyond just quote tick-sizes. As a result, all factors considered, many regional retail brokers continued to trade through the primary exchange, presumably because of several important best execution factors, beyond tick-size. These included greater depth of liquidity, better likelihood of execution and settlement, and consistency of competitive pricing opportunities.

Fair competition, tick-size harmonization and best execution

In 2020, the JFSA proposed the idea of updating Japan’s best execution policy to align it more closely with investor protection and transparency interests. As a follow-up to this, in December 2020 the JFSA launched a working group to discuss possible revisions to Japan’s best execution obligation for brokers.

On 2 June 2021, the working group published its report, calling for what we believe to be a perversely unfair best execution policy. Under this, PTS tick-sizes are required to be ‘cheaper’ than those of the TSE, and the proposed ‘price-focused’ best execution rule would require retail brokers to route their orders to the cheaper tick-size PTSs.

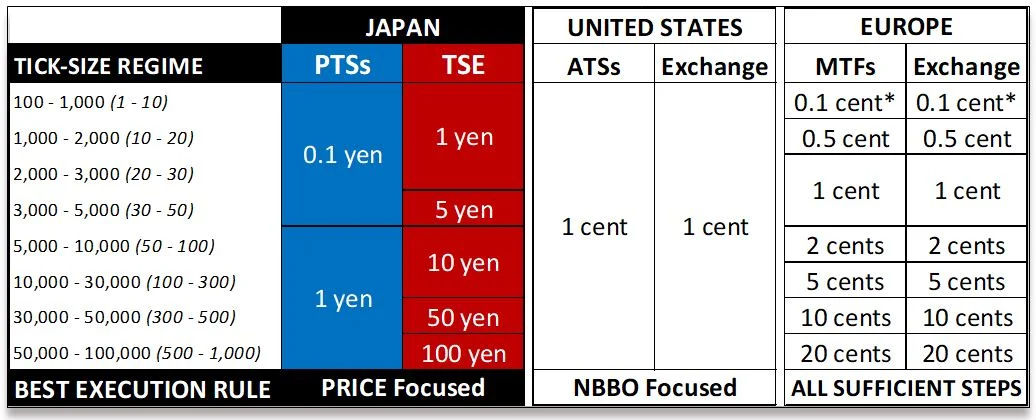

In other words, the JFSA is calling for a change in Japan’s best execution policy,[3] from the existing multi-factor ‘best terms’ approach to a single-factor, ‘price-focused’ approach for retail. However, this does not allow fair competition, as tick-sizes between the PTSs and exchanges are not harmonized. Quote tick-sizes are harmonized in the US and Europe, but not in Japan (see Figure 1). Japan’s existing ‘best terms’ best execution policy allows brokers to consider multiple factors when making order routing decisions. We believe that the proposed ‘price-focused’ best execution policy, which requires retail brokers to ‘comply or explain’ (although explaining carries a compliance burden), will eventually, when fully institutionalized, require brokers to route order flow to the PTSs based purely on tick-size difference, without considering other relevant best execution factors.

Figure 1: Tick-size regime and best execution rules compared[4]

Source: Chartis Research, AMF, JPX, Japannext, Chi-X Japan

PTSs can succeed without misaligned tick-size and best execution rules

PTSs are owned and operated by US financial powerhouses and have ready access to world-class trading technology and the most sophisticated artificial intelligence (AI) algorithms. This gives them an immense technology advantage over the TSE. In addition, PTSs‘ market-making partners are able to use ‘latency arbitrage’ to stay ahead of the information curve. This enables them to put their predictive analytics to work in providing investors with tighter bid-ask spreads. Some regulators have called for reduced latency arbitrage and other high-frequency trading (HFT) strategies. We don’t advocate this. We believe that a diversity of market participant types, strategies and investment time horizons supports best execution.

PTSs are authorized to operate both lit (transparent) and dark (non-transparent) trading venues, which the TSE is not authorized to do. This gives PTSs another competitive advantage over the TSE. While US and European regulators are actively seeking to force dark trading onto the lit exchanges, this is not the case in Japan. We are not advocating reduced off-exchange trading, as some regulators are. And we do not think a ‘trade-at’ rule promotes best execution. We believe that there is value in the price discovery process but that dark books also serve an essential best execution purpose by helping large institutional investors minimize costs related to order-information leakage.

PTSs also have a speed of innovation advantage over the TSE, by having greater flexibility and agility in offering new pricing structures. ‘Maker-taker’ approaches have proved very effective in helping off-exchange venues gain market share in the US. When the Better Alternative Trading System (BATS) introduced its ‘inverted’ pricing structure, for example, it gained significant US equity market share in just a few weeks. The US Securities and Exchange Commission (SEC) has called for a ban on these and payment for order flow (PFOF) pricing innovations, which has moved even more market share off-exchange. We don’t advocate banning inverted or PFOF price incentive schemes. We believe that there is room for these innovative structures, which aim to more finely calibrate risk metrics and information flows, provided that sufficient disclosures are made to clients, and clients have a choice between ‘all-in’ and ‘cost-plus’ pass-through pricing options.

Overall, we believe that PTSs have a wealth of competitive advantages over the exchanges that enable them to succeed without needing to ‘front-run’ the exchanges, via the combined effects of a misaligned tick-size regime and price-focused best execution rules. Regulators can and should support off-exchange trading and a diversity of investor types – even HFT. But there needs to be fair competition in the market structure across all participants. And certainly PTSs should not be given preferential treatment over the exchanges. Doing so may benefit PTSs, and their partners, but it will come at the expense of best execution and trust in Japan’s financial institutions.

[1] US quote tick-sizes are harmonized, but execution tick-sizes are not. In Europe, both quote and execution tick-sizes are harmonized. For more details, see the Chartis Research Pont of View article The US tick-size harmonization and optimization problem.

[2] ‘Exchanges’ here refers mostly to the TSE, because Japan’s other exchanges (Sapporo, Fukuoka and Nagoya), with a combined market share of less than 1%, are not significant competitors. For further discussion on Securities and Exchange Law and the ‘concentration rule’ change, see https://www.fsa.go.jp/p_mof/english/big-bang/ebb37.htm

[4] The EU tick-size table is expressed in Euro cents and covers average daily volume only of 2,000-9,000. For the purposes of comparison it has been made to fit the Japanese bands. For further details on EU tick-size regimes, see the AMF Report ‘MIFID II: IMPACT OF THE NEW TICK SIZE REGIME’.

The Japanese tick-size table excludes TOPIX 100 issues and covers share prices from 100 to 100,000 yen only, for the purposes of simplicity. The JFSA is proposing a ‘price-focused’ best execution policy, much like the National Best Bid and Offer (NBBO) approach in the US. Japan’s current best execution policy is a ‘best terms’ approach, much like the EU’s ‘all sufficient steps’ procedure-based approach. For ease of comparison, PTS tick-sizes represent the tighter of the two primary PTSs, Chi-X Japan and Japannext. For further details on Japan’s tick-size regime, see the JPX working paper ‘Impact of Tick Size Pilot Program on Trading Costs at Tokyo Stock Exchange’.

The US tick size table is expressed in US cents. For further details on the US tick-size regime, see the Chartis Research Pont of View article The US tick-size harmonization and optimization problem.

Points of View are short articles in which members of the Chartis team express their opinions on relevant topics in the risk technology marketplace. Chartis is a trading name of Infopro Digital Services Limited, whose branded publications consist of the opinions of its research analysts and should not be construed as advice.

If you have any comments or queries on Chartis Points of View, you can email the individual author, or email Chartis at info@chartis-research.com.

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@risk.net or view our subscription options here: http://subscriptions.risk.net/subscribe

You are currently unable to print this content. Please contact info@chartis-research.com to find out more.

You are currently unable to copy this content. Please contact info@chartis-research.com to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@chartis-research.com

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@chartis-research.com

More on Points of View

No surprises: 2025 will be another big year for AI

Last year was revolutionary for AI, with potentially far-reaching impacts, and 2025 looks set to offer more of the same, with perhaps some sobering lessons. Taking a pragmatic view, Maryam Akram, Research Principal at Chartis, offers some predictions for…

Regulatory reporting: deployment options and managed services

A collaborative article by Chartis and Regnology.

Reimagining Model Risk Management: New Tools and Approaches for a New Era

A collaborative report by Chartis and Evalueserve.

A New Regime: The Future of Private Credit and Risk Management Needs

A collaborative article by Chartis and RiskSpan.

Regulatory reporting: the transition from in-house to third-party systems

A collaborative article by Chartis and Regnology.

Keeping good company: streamlining client onboarding with CDI – Part 3

A collaborative article by Chartis and Encompass.

Keeping good company: streamlining client onboarding with CDI – Part 2

A collaborative article by Chartis and Encompass.

Keeping good company: streamlining client onboarding with CDI – Part 1

A collaborative article by Chartis and Encompass.