Moving to modular: developing a holistic anti-FinCrime system

A collaborative article by Chartis and AML Partners.

New systems, new benefits

Financial institutions worldwide are finding that by developing and bolstering their anti financial crime systems, they can move beyond the core functions of regulatory compliance and cutting admin costs. For many, effective financial crime prevention hinges on a holistic approach that accommodates vast amounts of data, and which incorporates a continuous and ongoing understanding of customer behavior.

To establish this type of holistic anti-financial crime system, financial institutions must implement its cornerstones: anti-money laundering (AML)/countering the financing of terrorism (CFT) tools and Know Your Customer (KYC) systems. These allow institutions to gain a deeper understanding of their clientele and their associated risks, and strengthen their ability to fight financial crime.

Orchestration platforms (like RegTechONE) can often serve as a unifying force for AML/CFT compliance solutions and KYC systems that employ a variety of data sources, technologies and risk management tools. These modular platforms can provide a centralized hub to enable firms to manage and analyze customer information and make important decisions in real time.

The advantages of a modular approach

A modular approach (such as that provided by RegTechONE) offers firms several important advantages, including:

- Cost-effectiveness. Financial institutions need only buy the modules they need, ‘a la carte’.

- Enhanced agility and scalability. Institutions can quickly adapt their processes to changing regulatory and organizational requirements. Modules can be added, removed or modified easily without affecting the overall system, often with low-code/no-code development capabilities.

- Reduced risk of errors. Modular systems are less prone to errors than monolithic systems, as each module is developed and tested independently, and changes to one module do not directly affect any others.

- Reduced time to market. By starting with a basic system and adding modules as required, institutions can reduce the time it takes to implement a new anti-financial crime solution.

Bringing it together: an integrated approach

An integrated approach to AML, CFT and KYC systems can give firms access to richer data via tools and processes such as behavior and transaction monitoring, customer due diligence (CDD) and KYC processes such as sanctions screening. These can help financial institutions achieve their organizational goals, enhance their customer satisfaction and improve their regulatory compliance. The key benefits of modular integration include:

- Enhanced risk detection and prevention. By integrating data from multiple sources, financial institutions can gain a deeper view of customer behavior and identify suspicious activity more effectively, helping to prevent fraud and money laundering before they occur.

- Reduced compliance costs. By automating AML/CFT and KYC processes and eliminating redundant data, financial institutions can reduce the costs associated with compliance.

- Improved customer satisfaction. By streamlining AML/CFT and KYC processes and reducing the need for manual review, financial institutions can provide a more seamless and efficient experience for customers, helping to attract and retain them.

- Improved data quality. By integrating data from multiple sources, institutions can ensure they have data that is accurate, complete and up to date.

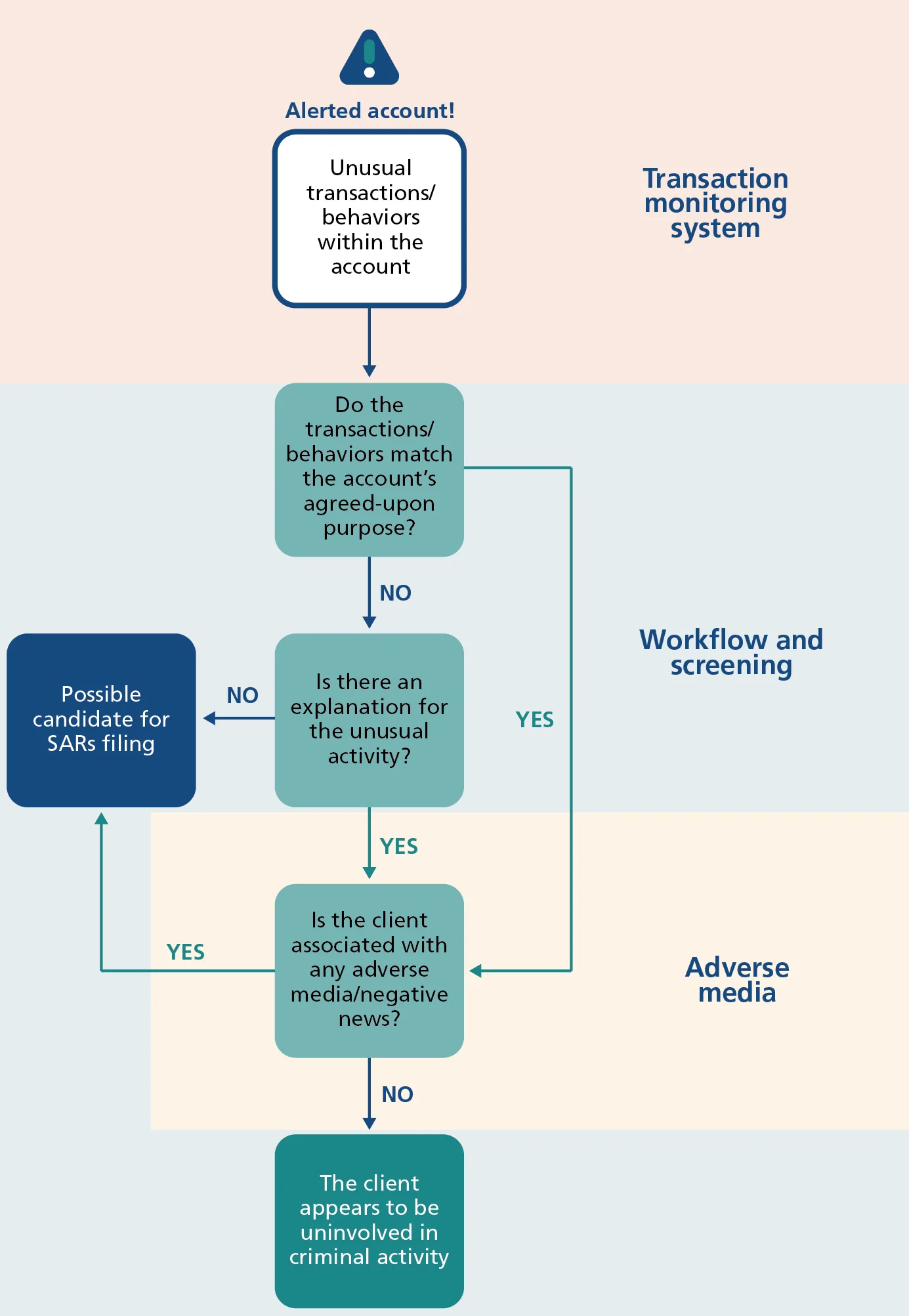

Integration in action: streamlining SARs

Financial institutions submit suspicious activity reports (SARs) to the Financial Crimes Enforcement Network (FinCEN) when they detect transactions or activities that they believe may be related to money laundering, terrorist financing or other illegal activity. The SAR is a critical tool in the fight against financial crime, as it gives law enforcement agencies valuable information about potential criminal activity.

Traditionally, SARs were filed manually by financial crime compliance teams. This process could involve several steps, including identifying suspicious transactions and behaviors, collecting information about them, completing a SAR form and submitting it to FinCEN.

With an integrated approach, firms can use technology to automate and streamline the SAR filing process (see Figure 1). This often involves the use of several elements:

- Transaction/behavior monitoring software to identify suspicious activity.

- The automatic collection of information from a variety of sources (internal or external).

- Pre-populated SAR forms and the automatic, electronic submission of reports to FinCEN.

Figure 1: Filing a SAR – an integrated system

Source: Chartis Research

The next step: AML Partners and integration

In today’s complex and interconnected financial landscape, a holistic anti-financial crime system that incorporates AML/CFT compliance solutions and KYC systems is vital for combatting fraud and AML activities. By leveraging tools and techniques such as transaction monitoring and CDD, often by assembling modular components, organizations can enhance their risk assessment, improve their risk detection and facilitate continuous risk monitoring. And by embedding this method of financial crime prevention, firms can also strengthen their customer relationships and competitive advantage.

AML Partners’ RegTechONE is a no-code platform that orchestrates AML/CFT compliance software and essential governance, risk management and compliance (GRC) solutions. RegTechONE is a single-solution risk-based application programming interface (API)-based platform with modules for CDD KYC, transaction monitoring, AML screening, FinCEN 314a, and vendor management.

RegTechONE’s no-code configurability allows end users to customize the platform to meet their compliance needs. The RegTechONE platform gives institutions the choice of implementing all modules, a few or a single one, allowing them to add extra modules over time in line with their evolving risk and compliance needs. RegTechONE modules are all integrated – information collected during customer onboarding and KYC activities feeds into the transaction monitoring and AML screening systems. RegTechONE’s no-code modules include:

- KYC and CDD. RegTechONE KYC integrates and automates every task required in CDD KYC. Features include:

- Customer onboarding (ID verification, document and information collection and verification).

- A multidimensional risk-processing engine that includes multiple modeling methods – weighted average and simple summation – that can be combined as needed.

- Watchlist and politically exposed person (PEP) screening, and the review of negative news and adverse media – all of which are integrated with risk.

- Registry for account principles/beneficial owners and related parties.

- Ongoing monitoring through perpetual KYC (pKYC) systems and options for electronic KYC (eKYC) golden records and hub-and-spoke monitoring.

- Reporting, analytics and automated periodic review/refresh.

- Behavior and transaction monitoring. RegTechONE’s Behavior and Transaction Monitoring module features rules, parameters, scheduling, integration of external tools and data, and dynamic case management for the fully integrated and time-saving working of cases.

- FinCEN 314a/subpoena screening. RegTechONE’s FinCEN 314a/subpoena screening enables the automated screening of customers’ names, related parties, principles, and transactional parties.

- Sanctions screening. This module automatically screens entities, customers, vendors and employees for PEPs, sanctions, adverse media and negative news. Using capabilities such as whitelisting, de-duplication and secondary screening, end users can drastically reduce false positive rates.

End users can also subscribe to AML Partners’ Risk Data Service (RDS) to receive regular updates on geographic risks that are vital to AML risk modeling and management. RDS includes country risk ratings and US-specific drug trafficking and financial crime data.

Overall, AML Partners’ RegTechONE is a versatile API-based platform that financial institutions of various sizes can use to meet their AML compliance and GRC needs. Offering ease of use, configuration and scale, it has a wide range of features and functionality to enable firms to adapt to changing regulations and industry best practices using this holistic, modular financial crime prevention platform.

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@risk.net or view our subscription options here: http://subscriptions.risk.net/subscribe

You are currently unable to print this content. Please contact info@chartis-research.com to find out more.

You are currently unable to copy this content. Please contact info@chartis-research.com to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@chartis-research.com

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@chartis-research.com

More on Custom Insights

Complacent RiskTech vendors are sleepwalking into a new, deregulated reality

Tectonic regulatory and legislative upheaval promises to transform financial institutions’ RiskTech spending. As compliance-based revenue streams slow due to deregulation, solution vendors will need to adopt more business risk-focused strategies for their product lines. Chartis Chief Researcher Sid Dash considers the likely impact of growing deregulation, and how vendors can prepare.

Regulatory reporting: deployment options and managed services

A collaborative article by Chartis and Regnology.

RiskTech100 2025 Winner’s Spotlight: Regnology

Regnology has secured the award for Regulatory Reporting in Banking, earned top honors in Supervisory Technology and ranked 22nd overall.

Reimagining Model Risk Management: New Tools and Approaches for a New Era

A collaborative report by Chartis and Evalueserve.

A New Regime: The Future of Private Credit and Risk Management Needs

A collaborative article by Chartis and RiskSpan.

Regulatory reporting: the transition from in-house to third-party systems

A collaborative article by Chartis and Regnology.

Keeping good company: streamlining client onboarding with CDI – Part 3

A collaborative article by Chartis and Encompass.

Keeping good company: streamlining client onboarding with CDI – Part 2

A collaborative article by Chartis and Encompass.